When valuation spreads, vacancy assumptions, and exit math conflicted, careful dialogue rather than leverage determined whether the RV park bridge-loan deal made sense.

There is a point in every nontraditional transaction when the spreadsheets stop answering the most important questions. The model may work. The appraisal may land within range. The debt service may pencil. Yet something deeper remains unresolved. It is not a missing data point, but an uncertainty about how an asset behaves, how a market functions, and how risk shows up over time.

That is where judgment begins.

This case study reflects one of those moments for 1892 Capital Partners. It was our second RV park loan and a reminder that familiarity with an asset class does not remove uncertainty. In many cases, it reveals how different two projects within the same category can truly be. This is a story about how lenders can approach deals in the absence of certainty and about how disciplined processes can replace rigid formulas when underwriting unique assets; in other words, when you’re underwriting in the dark.

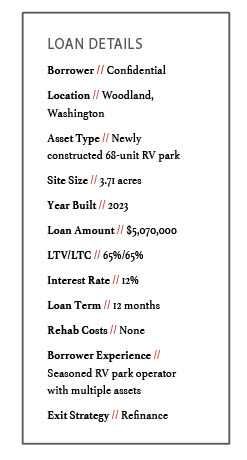

The Opportunity

This transaction came to us through one of our preferred brokers, Nick Klein of Bellevue Capital Group, alongside Dan Spurr—and this framing mattered.

The sponsor had recently completed construction on multiple RV parks with a clear institutional strategy in mind. Their plan was to aggregate the portfolio and refinance into a single permanent loan once stabilization was achieved. As construction loans reached maturity, the institutional lender unexpectedly changed its strategy and withdrew its commitment.

What had once been a clean, portfolio-level execution fragmented into several time-sensitive bridge financing needs.

In situations like this, speed alone is not a challenge. The real challenge is judgment. The sponsor did not need aggressive leverage or speculative capital; they needed a lender who could underwrite nuance and move quickly without compromising discipline. A rare combination, but precisely where relationship-driven execution becomes valuable.

Familiar Asset Class, Unfamiliar Risk

At first glance, RV parks were not new to us. Our portfolio already contained an RV park, and we’d spent significant time learning how the asset class performs across different regions.

But that familiarity created a false sense of comfort that we were careful to examine. RV parks are not homogeneous. They vary widely by location, tenant mix, length of stay, regulatory environment, and valuation methodology. Two assets that appear similar on paper can behave very differently in practice.

Green Flags That Earned the Right to More Work

Several early signals did not eliminate risk, but they earned the deal the right to deeper diligence. The property was brand new. The sponsor was experienced and had successfully developed multiple RV parks. The broker relationship was strong and credible. The leverage request was conservative.

These factors did not answer every question, but they did signal that the efforts to answer the remaining questions were worth making.

Location as the First Anchor Point

The turning point was geography. Although RV parks are recreational by nature, location largely determines how they function. Some are destination-oriented, with high turnover, heavier amenities, higher management intensity, and higher operating costs. Others operate as longer-term corridor assets, with lower turnover and leaner expense structures.

The property sits just off the I-5 corridor, a location that supports both transient demand and longer-term occupancy. That duality creates diversified income drivers and reduces reliance on any single tenancy pattern.

Location does not eliminate risk, but it provides context. In this case, it allowed us to frame the park as something more resilient than a purely seasonal or purely long-term asset, justifying deeper diligence rather than a quick rejection.

Red Flags That Required Real Work

Valuation and income assumptions remained the core areas of uncertainty throughout underwriting. Rather than trying to smooth those uncertainties away, we leaned into them. We compared performance patterns across markets. We overlaid our own conservative adjustments where the data felt fragile.

To test the appraiser’s assumptions, we engaged two experienced RV operators in different states. Each reviewed the project through a different lens, and that contrast sharpened our view and helped answer necessary questions about vacancy assumptions, management expenses, and how differently operators can experience the same market.

One operator evaluated the park from a destination-market perspective, forcing us to examine occupancy mix and turnover assumptions more closely. The park we were underwriting, however, was not a destination asset. It sat along a major travel corridor, supported longer stays, offered fewer amenities, and operated with a materially lower management expense ratio. Recognizing those differences allowed us to appropriately support a lower expense profile in underwriting rather than apply a destination-park cost structure where it did not belong.

The second operator came from a more competitive market with easier permitting and flagged vacancy assumptions as potentially low. That feedback led to deeper market diligence. What we found was limited competing inventory, significant permitting barriers, and constrained land availability, all of which supported lower vacancy expectations in this specific market.

The appraiser was a key part of this process. When asked to confirm assumptions, he was very helpful in providing supporting data around cap rate selection, pointing to high demand for RV inventory, scarcity of product, and the difficulty of permitting and constructing new parks. He also provided support for lower vacancy assumptions, citing current usage, the operator’s ability to fill any vacancies with either short-term or longer-term tenancies, and the fact the park is relatively new with highly desirable 50-amp service capable of accommodating larger and newer RVs.

Lastly, he helped confirm that a lower management expense ratio was warranted. The majority of sites were rented monthly, which requires less active management, and the park offered fewer amenities than destination-oriented RV parks, further reducing management intensity.

The Valuation Question That Would Not Go Away

RV parks can be valued on a fee simple or a leased-fee basis; the spread between those approaches is meaningful. In this case, that spread raised real questions about income durability, exit assumptions, and how future lenders would ultimately view the asset.

The difference between the leased-fee and fee simple valuations was nearly 15%, a material gap when determining value based on current leases. Given the longer-term tenancies in place, we believed it was more prudent to evaluate the asset based on the income being generated rather than a pro forma that assumed future rent increases.

In theory, rents can reset as tenants turn over. In practice, this park had no fixed 12-month leases and operated with a tenant profile that behaved more like long-term occupancy. We could have reached for a forward-looking valuation. Because the asset was still relatively new to us, we chose the more conservative leased-fee approach grounded in existing cash flow.

Structuring for Reality

This was a non-value-add bridge loan. Pricing reflected that reality.

Although the interest rate was lower than a typical value-add bridge, the diligence burden was meaningfully higher. The time invested was greater, and the internal debate was deeper.

We often discuss expectations with brokers early to ensure alignment.

One of the more notable structural decisions was omitting an interest reserve. Typically, we require one. In this case, the sponsor needed higher proceeds to stabilize their broader capital stack. The RV park could service debt, but the debt service coverage ratio at our rate would not satisfy most institutional lenders. We accepted that risk consciously and mitigated it elsewhere.

We underwrote the refinance exit at a lower loan-to-value than the bridge. That conservative exit assumption materially improved the probability of a successful takeout and aligned incentives across all parties.

Risk is not eliminated by avoiding it. It is managed by placing it where it can be absorbed.

Loan Closing and Current Status

The loan closed as the project stabilized and began optimizing rents toward the highest and best use. There were no construction draws. No execution risk remained. Performance responsibility rested with the sponsor, where it belonged. To date, the borrower has met expectations, and the asset has performed as underwritten.

The hardest part of this transaction was trusting people, not the math. We had to trust the broker to present the deal honestly and the appraiser to engage thoughtfully. We also had to trust operators to share real experiences rather than sales narratives.

This deal reinforced an important belief. Brokers invest years building trust with sponsors. A lender’s role is not to disrupt that dynamic but to support it. We aim to stay in our lane, execute, preserve relationships, and allow brokers to remain the primary advisors while we provide the capital and judgment behind the scenes.

The Evolution

Markets change, asset classes evolve and institutional capital shifts strategies. In a constantly changing environment, a deal does not need to fit a formula; it just needs to make sense.

We continue to test new asset classes, identify financing gaps, and reassess risk and reward in real time. If the value is real and the risk is understood, many conventional overlays simply do not apply. This RV park was not a replication of our first. It was a reminder that experience sharpens awareness of uncertainty.

Underwriting in the dark is about building enough perspective, process, and humility to move forward responsibly when the answers are incomplete.

Leave A Comment