KBRA’s entrance into rental transition loans ratings introduces optionality that could materially reshape tranche sizing, pricing, and proceeds.

This is year, getting the best financing for Residential Transitional Loan (RTL) portfolios will require more deliberate planning than in prior years. It’s not because of a lack of investor demand or market fundamentals have shifted. It’s because, for the first time, lenders have a real choice in how these loans can be securitized and rated.

On Feb. 2, KBRA released its proposed methodology for rating bonds backed by RTL loans. It is worth considering what the arrival of a second credible rating agency means for private, nonbank lenders active in the RTL space.

To understand why this matters, it helps to step back and simplify how RTL securitizations work. Lenders originate short-term residential bridge loans, pool them, and then issue bonds backed by the cash flows from those loan pools. Those bonds are divided into tranches, or slices of risk represented by a percentage of the deal, that determine who gets paid first. The senior slice receives principal first and is, therefore, viewed as the safest.

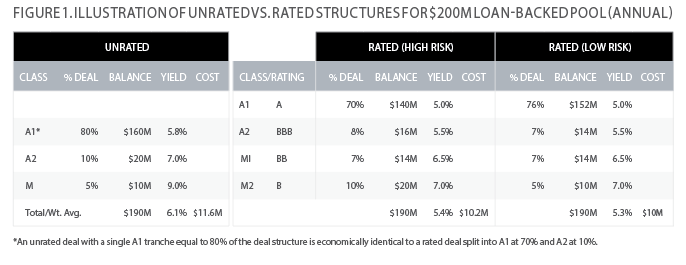

Importantly, tranche labels can make structures appear different even when the economics are the same. For example, an unrated deal with a single A1 tranche equal to 80% of the deal structure is economically identical to a rated deal split into A1 at 70% and A2 at 10%. Although the names differ, the senior exposure still totals 80% of the deal.

Before 2024, issuers were effectively structuring to a single dominant unrated approach, with predictable tranche splits (e.g., 80%, 10%, and 5% for A1, A2, and M classes, respectively). Outcomes were predictable. Execution risk was low. But flexibility was limited.

That changed when DBRS rated the first RTL securitization, Toorak 2024-RRTL1, in February 2024, a turning point for the asset class. The entrance of a rating agency into the RTL market formalized risk assessment and tranche sizing based on perceived collateral performance. By assigning investment-grade ratings (BBB and above), rating agencies influence pricing, investor eligibility, and the leverage a lender can achieve.

Investment-grade ratings on bonds backed by RTL loans opened the door for institutional investors expanding the bond buyer base from a few dozen investors with pockets of money for unrated securities to include over 100 investors, such as insurance companies, which require investment-grade bonds.

The higher demand for rated bonds drove down the overall pricing by as much as 100 basis points, resulting in material cost savings of hundreds of thousands of dollars per transaction. Figure 1 shows an example of unrated versus rated structures in a $200 million loan-backed pool.

Since then, DBRS has developed a deep understanding of how RTL loans perform, having rated nearly 30 deals from 15 issuers for more than two years. That experience allows DBRS to consider a more nuanced portfolio, including wider ground-up compositions, giving issuers access to a proven methodology that has been tested in practice.

KBRA’s announcement that it intends to rate RTL securitizations as early as the second quarter does not represent the same disruption. Instead, it brings an alternative analytical lens, using a different but still institutionally accepted rule book.

Importantly, KBRA may perceive certain collateral attributes as different risks than DBRS, resulting in materially different pool-level conclusions. Collateral pools that were historically viewed as higher risk under DBRS assumptions may be viewed as lower risk by KBRA, enabling higher senior tranche percentages against specific collateral profiles and making those structures a better fit for certain investor portfolios.

Issuers are no longer implicitly structuring a single methodology. That new flexibility brings opportunity. It also introduces a new responsibility: Someone must decide which framework best aligns with the portfolio’s characteristics. Even modest differences in assumptions can translate into real dollars at execution.

There is no universally “right” rating agency for each issuer. The answer depends on collateral composition, loan size distribution, extension behavior, how different agencies view those attributes as risk, and exposure to small multifamily assets. Getting that answer right may require more upfront analysis this year, but the payoff can be meaningful.

For lenders willing to engage in comparative analysis, this creates an opportunity to optimize execution rather than default to convention.

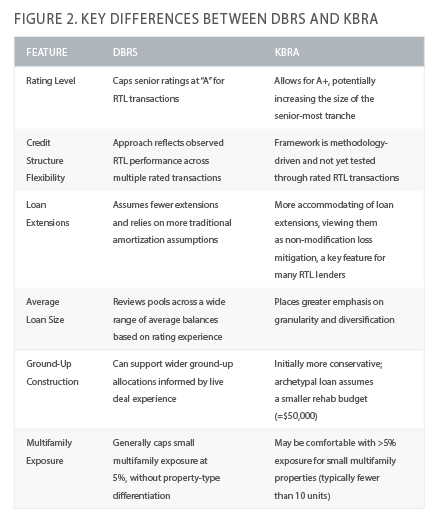

DBRS vs. KBRA

At a high level, both rating agencies cap RTL securitizations at the single-A level. However, there are some key differences in their approaches that issuers should consider (see Fig. 2).

One meaningful distinction is that KBRA’s framework allows for an A+ rating at the top of the capital stack, which may increase the size of the senior tranche and improve advance rates for certain portfolios.

DBRS generally caps ratings at “A” but offsets that limitation with structural flexibility informed by live transaction experience.

Further, the archetypal pool assumed under KBRA’s methodology appears more accommodating to portfolios with smaller average loan sizes, smaller rehab budgets, and more frequent extensions. Small differences in loss assumptions, property-type treatment, or loan-size weighting can shift subordination levels by tens of basis points, resulting in hundreds of thousands of dollars in proceeds per deal.

Over multiple transactions, those differences compound. Lenders that securitize regularly will feel the impact in execution consistency and overall cost of capital.

This is why upfront modeling matters more now than it did when there was effectively only one expected outcome.

Rethinking Small Multifamily in RTL

Under existing DBRS-rated frameworks, multifamily exposure has generally been capped at 5%, partly due to internal rating-agency processes that involve CMBS counterparts and do not meaningfully differentiate between small and large multifamily properties.

According to conversations with KBRA, their methodology may allow up to 10% exposure to small multifamily properties with fewer than 10 units.

This distinction is meaningful. Sub-10-unit properties often behave more like two-to-four-unit residential assets than traditional commercial multifamily. They are typically financed, underwritten, and sold based on comparable sales rather than capitalization rate analysis and are often backed by the same borrower base as traditional residential investors.

By acknowledging that distinction, KBRA may create additional flexibility for lenders whose originations naturally include slightly larger residential buildings that function as residential housing stock.

For platforms operating in dense urban and infill suburban markets—such as New York and New Jersey—where small multifamily properties represent a significant share of supply, this adjustment could materially improve securitization execution.

Getting It Right

In this environment, the strongest advantage belongs to lenders whose capital markets teams or external advisors proactively evaluate rating agency fit before a deal is launched.

That means testing collateral under multiple methodologies, understanding how portfolio construction affects tranche sizing, aligning origination strategy with long-term financing goals, and avoiding late-stage surprises that slow execution or weaken pricing.

That choice introduces a need for more intentional planning, particularly in 2026 as the market adjusts to multiple viable rating approaches. Lenders who compare options, understand their portfolio’s natural fit and align execution strategy accordingly are more likely to achieve better advance rates, broader investor participation, and more predictable outcomes.

Simply put, the lenders who do a bit more work upfront this year are positioning themselves for cheaper, more reliable capital in the years ahead.

The bottom line is simple. RTL demand is still there. Institutional capital is still available. What has changed is that lenders now have to be more intentional. Those who embrace that shift rather than resist it are likely to secure better advance rates, broader investor participation, and more scalable securitization programs over time.

Leave A Comment