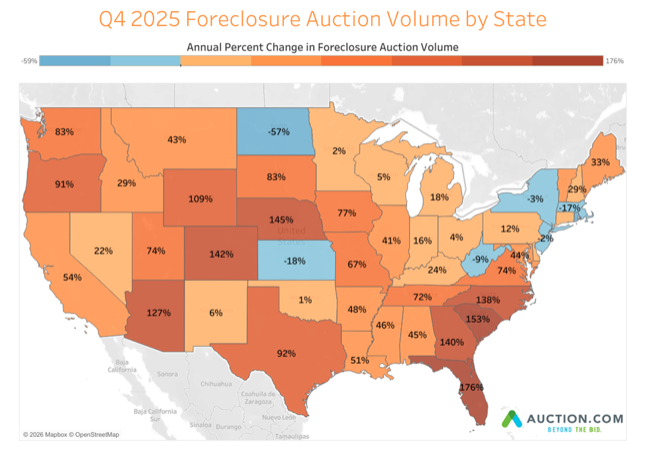

Bidding activity at foreclosure auctions provides early clues to 2025’s real estate market winners and losers.

Bidding trends at foreclosure auctions in late 2024 indicate which local markets are likely to see gains or losses in retail home prices in 2025.

“Higher home prices with an inevitable price drop coming in the near future,” speculated an Auction.com buyer from Indiana in a January 2025 survey. “(I am) spending less because prices will drop and [it] makes no sense to buy when you know prices will drop even further.”

In aggregate, the bidding behavior of distressed property auction buyers like this one help signal which markets are likely to “win” in 2025 and which markets are in danger of seeing a slowdown in home sales and home prices.

That’s because the local community developers who are the biggest buyers at distressed property auctions know their local markets as well as or better than anyone. Their success hinges on accurately predicting what their local market will look like about three to six months in the future—the typical time it takes them to renovate distressed properties and return them to the retail market as resales or rentals.

“Going into the New Year, I do feel that the market will improve and as such if the home can be bought at a reasonable price, I’m a buyer,” wrote an Auction.com buyer from Texas in the January survey.

The key auction bidding behavior metrics that signal likely local market winners and losers in 2025 are the sales rate at foreclosure auction—the share of auction properties that sell—and the ratio of winning bid to estimated after-repair value at auction.

The sales rate indicates quantity demand from local community developers—the quantity buyers are willing to buy. The winning bid-to-value ratio indicates price demand from local community developers—the price buyers are willing to pay.

Markets Most Likely to Win

Markets likely to win in 2025 are those in which both the quantity demand and the price demand rose in the fourth quarter of 2024 compared to a year ago, ordered by highest to lowest quantity demand.

Of 63 local markets analyzed in the Auction.com data, 19 (30%) fit the category of likely winners in 2025, primarily markets in the Northeast and Rust Belt and parts of the Midwest, with a few notable exceptions such as Portland, Oregon, and New Orleans (see Fig. 1).

“High demand for turnkey properties in the D.C. metropolitan area,” wrote one survey respondent from Maryland. “The high interest rates will drastically effect marketability though.”

Markets in Danger of a Downturn

Conversely, markets in danger of a housing downturn in 2025 were those in which both quantity demand and price demand declined in fourth quarter 2024 compared to a year ago, ordered by the lowest to highest quantity demand.

Out of the 63 local markets analyzed, 16 (25%) fit the category of likely losers in 2025, primarily markets in the Southeast and Sun Belt, although there were several notable exceptions (see Fig. 2).

“Cost of goods to rehab are up so need better spread,” wrote one survey respondent from Texas.

The signals for 2025 were less clear in the remaining 28 markets analyzed, with quantity demand and price demand going in opposite directions in fourth quarter 2024.

Headwinds and Tailwinds

This aligns somewhat with the results of the Auction.com buyer survey, which shows that local community developers buying distressed properties at auction still view market conditions as more of a headwind than a tailwind for their real estate investing activity.

Twenty-four percent of survey respondents said market conditions are making them more willing to buy while 35% said market conditions are making them less willing to buy. The remaining 41% said market conditions are not impacting their willingness to buy.

Buyers surveyed cited higher acquisition costs, higher rehab costs, and unfavorable mortgage rates as the top three market conditions making them less willing to buy distressed properties at auction.

“Number 1 is interest rates affecting my holding costs and mortgage,” wrote one survey respondent from Maryland, who said market conditions are making him less willing to buy. “I buy properties at auction, fix them up, then rent them out, and refinance them into a mortgage and hold the property, so interest rates (are) everything to me. “However, if I get a good purchase price, I can deal with high interest rates,” he added.

Lower prices may offer the best opportunity for buyers to increase their purchases at auction. Given recent guidance from the Federal Reserve, the prospect of dropping mortgage rates in 2025 is becoming more unlikely. Threats of tariffs and deportations from the Trump administration point to rising renovation costs, both for materials and labor.

“More affordable and cheaper homes will help increase bidding,” wrote one survey respondent from Texas, who said market conditions are making him less willing to buy.

On the other side of the coin, a strong fix-and-flip market, low retail inventory, and lower acquisition costs were the top three market conditions making buyers more willing to buy distressed properties at auction.

“The price of everything has increased, including foreclosures,” wrote one survey respondent from Maine, who said market conditions have not impacted his willingness to buy. “However, as long as profit margins stay the same, it doesn’t affect me much.”

The fix-and-flip market has been waning in many parts of the country due to slowing home price appreciation and low inventory of distressed properties available for value-add investing. But that’s not as much the case in many Northeast and Rust Belt markets where home price appreciation is outperforming the national average and where more distressed, value-add buying opportunities tend to be.

Home Prices and Foreclosure Inventory

According to data from the ICE Mortgage Monitor Report published in February 2025, the top five markets for fastest annual home price appreciation in December 2024 were all in the Northeast or Rust Belt: Buffalo, New York; Hartford, Connecticut; Providence, Rhode Island; Cleveland, Ohio; and Detroit, Michigan.

“My investing strategy is always powered by market value fluctuations, builder costs, and inventory,” wrote one survey respondent from Nevada, who said market conditions are not impacting her willingness to buy.

Meanwhile, according to Auction.com data, four of the top five markets with the highest volume of properties brought to foreclosure auction in fourth quarter 2024 were in the Northeast or Rust Belt: New York, Chicago, Dallas, Detroit, and Philadelphia.

“I’m finding more foreclosure properties on which to bid,” wrote one survey respondent from New York, who said market conditions are making her more willing to buy.

A similar regional pattern shows up in retail market inventory (see Fig. 3). Although retail market inventory is rising in most markets across the country, it’s not rising as rapidly in many parts of the Northeast and Rust Belt. Data from Realtor.com shows that among metro areas with at least 2,500 active listings in January 2025, those with the biggest annual increase in listing inventory were Denver, Las Vegas, Tucson, San Diego, and Naples, Florida. Metros with the smallest increase in active listing inventory were New York, Boston, Cleveland, Chicago, and Minneapolis.

Leave A Comment