A modest sentiment lift among distressed buyers at year-end suggests movement in the housing market in early 2026.

Thee sentiment and bidding behavior of local community developers buying distressed properties at auction increased slightly in late 2025 as available inventory picked up and pricing drifted lower, indicating a possible rebound in the retail housing market in early 2026.

“Higher foreclosures and lower prices motivate me to buy,” wrote one buyer from Arizona in response to a fourth-quarter Auction.com 2025 buyer survey.

This buyer’s perspective reflected gradually rebounding sentiment in the fourth quarter among the local community developers buying distressed properties at foreclosure and bank-owned (REO) auctions. These local community developers collectively are a good barometer of housing market health, given their success depends on accurately anticipating what the local real estate market will look like in the next three to six months—the time it typically takes to renovate distressed properties and return them to the retail market as resales or rentals.

“How long a house bought at auction stays on the market after it is ready to sell,” wrote Oregon-based survey respondent Christine, explaining how retail housing market conditions impact her willingness to buy at auction. “The longer on market the fewer houses can be purchased (at auction).”

The Auction.com buyer sentiment index, calculated based on a series of the same five questions asked of active buyers each quarter, increased to 49.94 in fourth-quarter 2025, up from 49.92 in the previous quarter and unchanged from a year ago. It was the highest index reading since the first quarter of 2025, when buyer sentiment surged on the heels of the presidential election before dipping again in the second and third quarters as tariffs were announced and took effect (see Fig. 1).

Willingness to Buy

Although at a three-quarter high, the buyer sentiment index below 50 indicates buyers who are still more cautious than they are aggressive when it comes to distressed property purchases. Thirty-six percent of survey respondents said they were less willing to buy due to current market conditions, well above the 19% who said they were more willing to buy but still down from 38% in the previous quarter. The 19% more willing to buy was unchanged from the previous quarter.

Meanwhile, 45% of survey respondents said current market conditions are not impacting their willingness to buy, up from 42% in the previous quarter and unchanged from a year ago.

“I make decisions based on the activity within the specific area that I’m looking to purchase,” wrote Stacey, an Illinois-based survey respondent. “There are some areas that are still thriving regardless of what is happening at the federal level.”

Price a Primary Driver

Higher property acquisition and rehab costs were far and away the primary reasons buyers gave for being less willing to buy, with 56% selecting higher acquisition costs and 51% selecting higher rehab costs (labor and material). The next highest reason was a weak fix-and-flip market, selected by 26% of buyers surveyed.

“I am buying more to hold and rent than I was before (when) I was buying to flip and sell,” write Lane, an Auction.com buyer in Minnesota.

Conversely, 45% of buyers surveyed said lower property acquisition costs were making them more willing to buy, by far the highest reason given for being more willing to buy. The high share of buyers both more willing and less willing to buy due to either falling or rising acquisition costs reflects the varying local housing market conditions across the country.

Divergent Home Price Trends

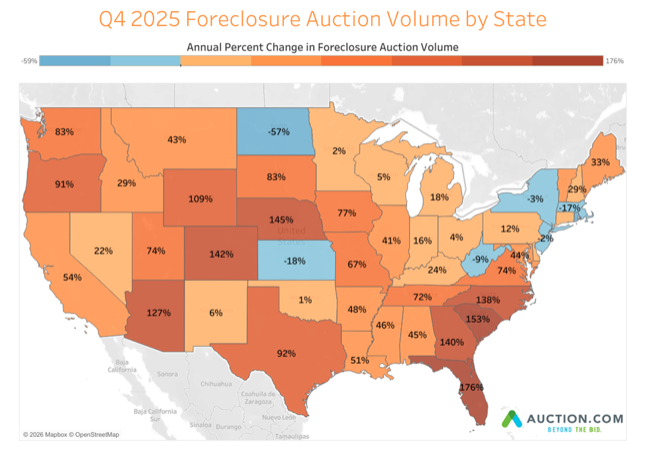

Data from ICE shows that about one-third of local markets have experienced a home price correction of at least 1% since 2022, most of those in the Southeast and West. Notable markets include Austin, Texas (22% correction); Cape Coral-Fort Myers, Florida (15% correction); San Francisco, California (9% correction); Phoenix, Arizona (7% correction); and Denver, Colorado (6% correction).

“The primary concern is the growing number of houses for sale,” wrote survey respondent Kevin from Arkansas. “This creates a buyers’ market; therefore, you can expect to sell a property for less than you would have a year ago.”

By comparison, many markets in the Midwest and Northeast have not experienced a home price correction and continued to report relatively strong home price growth into late 2025. Notable markets with strong price growth in September 2025 included Rochester, New York (up 8% annually); Philadelphia (up 8%); Milwaukee (up 6%); Chicago (up 6%); and Cleveland (up 5%).

“Local market supply versus demand,” wrote Connecticut-based survey respondent Mark, who said he planned to buy more properties at auction in the next three months than he did during the previous three months. “My decisions are based upon competing inventory.”

Property Purchase Plans

Both the still-strong housing markets in the Midwest and Northeast, as well as the growing number of price-corrected housing markets in the Southeast and West, may be giving auction buyers some comfort that the housing market is not teetering on the precipice of a cliff, about to crash. That was evident in the lower percentage saying the market was making them less willing to buy and also in a growing share who said they planned to buy the same amount or more properties at auction in the next three months compared to what they purchased in the previous three months.

Eighty-three percent of Auction.com buyers surveyed in fourth-quarter 2025 said they planned to buy the same amount or more properties in the next three months, up from 79.8% in the previous quarter and 79.5% a year ago. By comparison, 17% said they planned to buy fewer properties in the next three months, down from 20% in both the previous quarter and a year ago (see Fig. 2).

Buyer and Seller Pricing

Still, buyers indicated they are still being relatively cautious about what they are willing to pay for distressed properties purchased at auction, with 23% surveyed saying they are bidding lower due to market conditions over the last 90 days — unchanged from the percentage who said that in the previous quarter and a year ago. Meanwhile, only 1% said they are bidding higher, down from 3% in the previous quarter, although unchanged from a year ago.

“Bidding lower prices to hedge for declining prices and climbing inventories,” wrote survey respondent Scott from Texas.

The good news for buyers bidding lower at auction: The banks and mortgage servicers selling at auction are also lowering pricing. The average credit bid-to-after repair value ratio for properties brought to foreclosure auction in third-quarter 2025 was 61.5%, down from 62.5% in the previous quarter and down from 62.3% a year ago, according to proprietary Auction.com data (see Fig. 3). The credit bid at foreclosure auction functions as the reserve—the minimum price the seller is able or willing to take. The after-repair value is the estimated value of the property in fully renovated condition.

REO auction sellers also lowered pricing in the third quarter of 2025. The average reserve-to-after repair value ratio at REO auction was 65.9% in third-quarter 2025, down from 67% in the previous quarter and down from 68.2% a year ago.

Leave A Comment