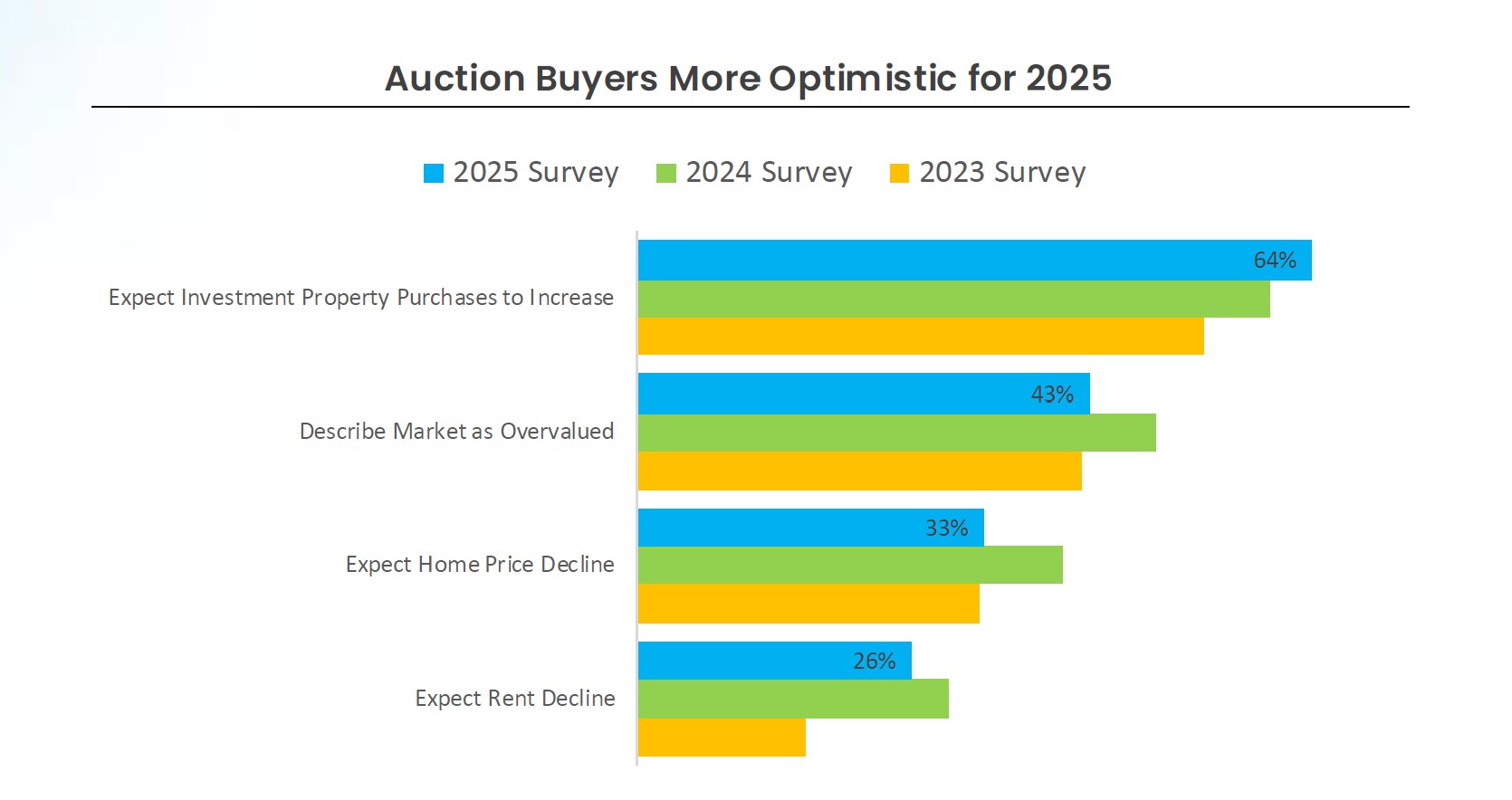

This article was co-authored by Michael Fogliano, Forecasa, and Sean Morgan, Forecasa.

Although still below the highs of Spring 2022, the private lending market has shown signs of recovery in the first half of 2024.

In aggregate, the private lending market still isn’t near its spring 2022 highs, but it has been gaining steam through the first half of 2024. When removing loans greater than $5 million, the private lending industry has originated nearly $50 billion in the first two quarters of 2024. May 2024 was a high watermark for private lending originations since June 2022, recording more than 21,000 transactions. That trend did not continue in June 2024óthe industry saw a 16% contraction. That being said, Forecasa does expect July 2024 to rebound from the lull in June (see Fig. 1).

As you can see in Figure 2, non-private (conventional lending) has followed the same trend as private lending throughout the first half of 2024. Non-private lending has a more significant gap to close versus private lending but is moving in the right direction. As interest rates continue to decline, Forecasa expects this trend to continue.

Biggest market movers

Forecasa evaluated the private lending originations in all major MSAs. The information below highlights the areas with the largest increases and the largest decreases in total number of private lender originations from year-to-date 2024 versus year-to-date 2023.

Largest Gains

- Birmingham-Hoover, AL (76%)

- Macon-Bibb, GA (72%)

- Montgomery, AL (61%)

- San Diego, CA (42%)

- Spartanburg, SC (42%)

- Winston-Salem, NC (40%)

- Mobile, AL (36%)

- Chattanooga, TN (33%)

- Myrtle Beach, SC (32%)

- Stockton-Lodi, CA (32%)

Largest Losses

- Spokane, WA (-28%)

- Killeen-Temple, TX (-28%)

- Atlanta, GA (-24%)

- New Orleans (-24%)

- Tucson, AZ (-19%)

- Baltimore, MD (-18%)

- Dayton, OH (-18%)

- Port St. Lucie, FL (-18%)

- New Haven, CT (-17%)

- Indianapolis, IN (-15%)

The Southeast region of the country showed the highest number of gainers followed by California. Outside of San Diego, the remaining MSAs with the largest gains were Tier II and Tier III markets. Among the MSAs that saw the largest losses, four of them were Tier I markets – Atlanta, New Orleans, Baltimore, and Indianapolis.

Product mix analysis

Forecasa has identified more than 6,200 private lenders originating mortgages since 2021. Although these lenders are all classified as private lenders, they are not all the same. They offer different products, originate in different areas, target different customer bases, and have different capital market strategies.

Since 2021, private lending has trended to be mostly short-term loans (i.e., originations with a maturity of five years or less). In the first two quarters of 2024, 59% of loans originated were short term (see Fig. 3). However, there is still a minority of lenders that remain focused on long-term loans. In 2024, 11 % of the active private lenders originated long-term loans exclusively, and 23% have originated some number of long-term loans. There has also been an increase in long-term DSCR loans being offered by more traditional non-QM lenders like NewFi, A&D Mortgage, United Wholesale, and others.

Average mortgage amount

Figure 4 shows the average mortgage amount of loans by quarter by term. Long-term loans typically have smaller average mortgage amounts as there is limited/no construction budget built into the loan. It also makes sense that the longer-term loan average has dropped as lenders pull back on leverage ratios. Short-term average loan amounts have remained relatively flat.

Private lending loan performance

To measure private lending loan performance, Forecasa has started tracking negative remarks (notice of defaults, notice of trustee sales, lis pendens, foreclosures) filed by private lenders compared to private lending originations. As Figure 5 notes, this ranges from 4.12% to 5.05%, with an overall of 4.64% for year-to-date 2024. Private lending loan modifications in the first two quarters saw a slight increase (<5%) when compared to the first two quarters of 2023.

Michael Fogliano is a product manager at Forecasa, responsible for product development and data analysis. After studying mathematics, Fogliano gained experience in several industries, always working with complex data.

Michael Fogliano is a product manager at Forecasa, responsible for product development and data analysis. After studying mathematics, Fogliano gained experience in several industries, always working with complex data.

Sean Morgan is the founder and CEO of Forecasa, where his primary focus is product and business development. He has experience in oil and gas intelligence, and he began his career as a CPA for PwC, cultivating a strong foundation in data interpretation and strategic insights.

Leave A Comment