Time is of the essence with foreclosures. Being familiar with the procedures involved will save you time and make the process smoother.

Your borrower has not paid their $1,000,000 mortgage note receivable for three months. You, therefore, decide to foreclose on the loan. But you haven’t performed a foreclosure in the past, so you need to determine the appropriate operational procedures.

Foreclosures are a laborious process and can take anywhere from 120 to 180 days to complete. Beginning the process as soon as possible is critical. Many private equity fund managers start the process immediately after a borrower has been delinquent for 30 or more days. The first step is to discuss the issue with legal counsel, who will determine the appropriate foreclosure laws for the state in which the foreclosure will occur. Once legal counsel has informed you of the applicable laws, you will be ready to take action.

Although foreclosure laws vary from state to state, there are some commonalities to the process. We’ll use a case study to illustrate them.

Determining Fair Value

The foreclosure process will involve a public auction. Before the public auction day, you have to set a minimum bid price; most people set it at par value. Once the property goes to auction, you will have one of two outcomes: the property will either be sold or it will revert to you at the bid price.

From an accounting standpoint, you need to convert the mortgage note receivable to a real estate-owned property (REO). Fortunately, whether your accounting policies require that you use the accrual (cost or fair value) or income tax accounting treatment, the outcome will be the same. Specifically, the property will need to be marked to fair market value, which is obtained through either a valuation report from a credentialed valuation expert or a broker’s price opinion report. Before you decide to invest in either, check with your CPA because they may have specific requirements regarding the type of report that you need.

An auditor will also inquire about the overall valuation reasonableness test(s) performed to ensure the property valuation is reasonable. Using residential property as an example, you could start by cross-checking the property valuation against major real estate databases such as Zillow and Trulia. Alternatively, an independent cash flow analysis can be performed to determine whether your fair value assessment is similar to the valuation received. For example, the valuation received for the property in this example was $1,400,000.

Determining Commission

The next step in the process is to determine the appropriate commission to sell the property. Using a rate of 5%, the commission expense would be deducted against the fair value of the property. The fair value, net of estimated cost to sell (net realizable value), would be $1,330,000 ($1,400,000 less commission of $70,000).

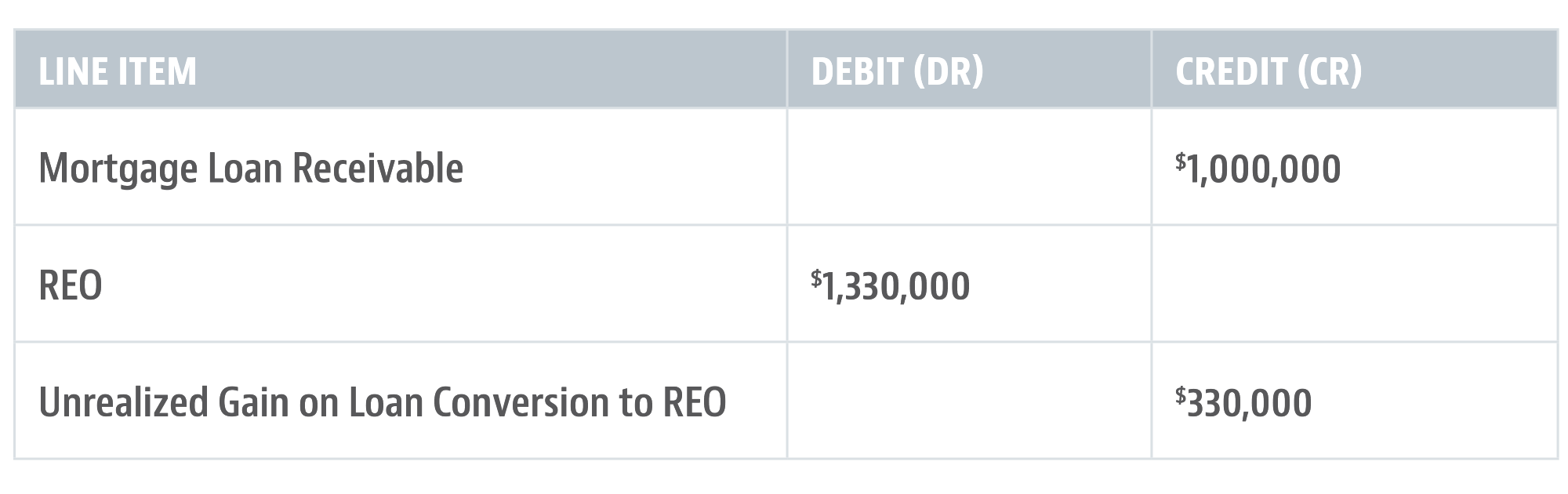

Creating an REO Receivable

The next step is to reduce the book value of the mortgage loan receivable plus any accrued interest receivable to create an REO receivable for the net realizable value of the property. The difference, in this case, is recorded as an unrealized gain on the property, and the entries on the balance sheet and profit and loss statements would be reflected as follows:

It is important to note that several different scenarios exist with the REO at this point, and a different accounting treatment will need to be employed for each of the following scenarios:

Scenario 1. Additional costs may be required to bring the REO to completion. Under this scenario, you will be required to capitalize the additional costs of construction but will also be required to periodically compare the book value of the REO with its fair value to determine whether the asset is impaired.

Scenario 2. The REO may be sold as is. Under this scenario, you will only be required to record the final transaction with a realized incremental gain or loss on the sale.

Scenario 3. The REO may be held for investment and rented. Under this scenario, the property will have to be depreciated.

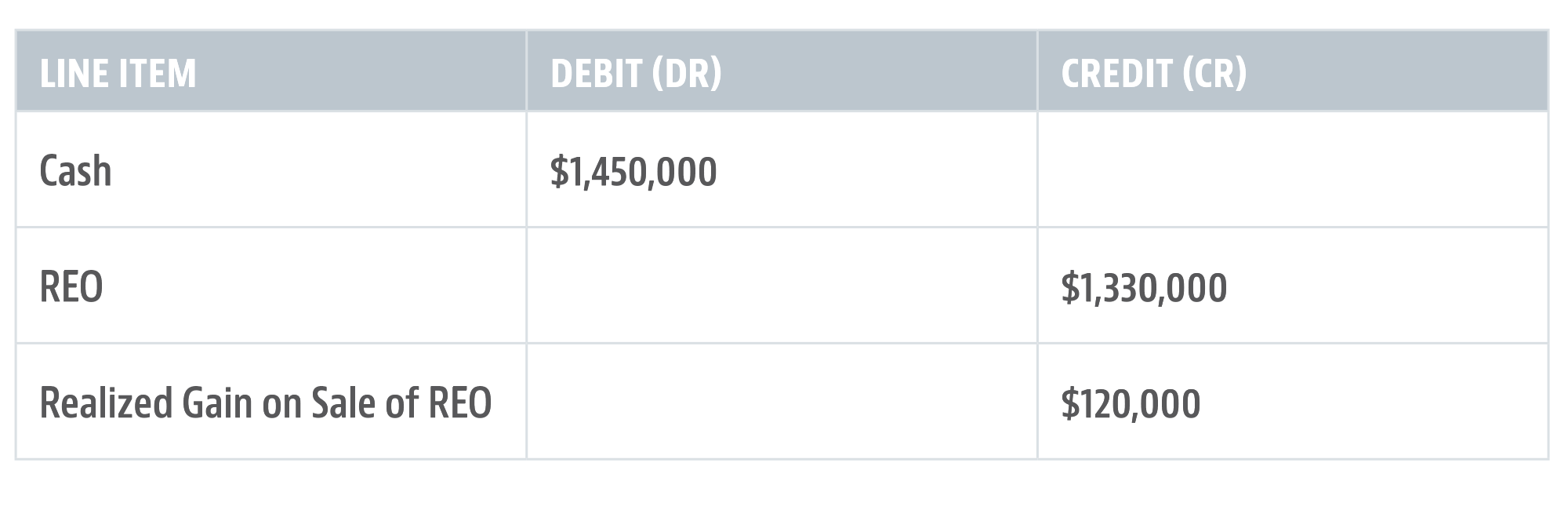

Ultimately, for this particular property, you decided to sell it as is. You received a post-commission offer of $1,450,000. The correct entries to complete this transaction are as follows:

REO transactions can be complex, and various other variables can change your strategy about how to dispose of and account for them. Consulting with the appropriate professionals is prudent.

Leave A Comment