Want more resources to help you manage the COVID-19 pandemic?

Here's how 2020 is shaping up for private lenders.

What is the state of the private lending industry in the U.S.?

Unlike the national housing market, there is no such thing as a national private lending market. There are 392 defined Metropolitan Statistical Areas (MSAs) in the country. If you consider the distribution of the remaining regional economic markets outside those MSAs in the 50 states, you end up with 501 unique regional and local markets. Each has its own unique characteristics and performance metrics.

So, while it's important to understand trends. everyone in the private lending industry should approach the question about the state of the industry differently.

Think More Narrowly

First, they should ask, "What is the state of the regional markets I play in? Most importantly, what are the key differences and how I should adapt to those markets?

Products, rates, prices and economic trends vary widely. For example, if you are in Memphis, you may want to know the local differences from one street to another. But, if you are in Kansas City, you want to consider a flat set of fees that makes the deal economics in a stable market make sense. In Eugene, Oregon, the metric shifts to Dutch construction and rehab economics.

Given those dynamics, focus on the most accurate actionable data that is based on the metrics for a targeted MSA or a state.

Looming Recession?

With fast developing events at the time of this update, markets around the world have frozen and COVID-19 is creating stock market disruptions. It is natural for credit providers in turbulent cycles to freeze credit and for liquidity to disappear. Make no mistake, without major governmental bailouts around the world, the global economy will shrink by 22%. Some even estimate by 35%.

Impacts on Private Lending

Here's what's happening with lenders as a result of the market turmoil:

- Loan aggregators who receive most of their funds from the institutional channel are feeling the pressure to freeze liquidity and, indeed, most seized or significantly slowed down.

- Secondary market loan aggregators funded by Wall Street and institutional funds have already tightened their underwriting guidelines.

- Draw requests to complete existing projects accelerated. In fact, we are seeing a 183% increase in that area.

- Construction is classified as an essential business and can stay open in many states, so rehab fix–and–flip and construction continues.

- Private local and traditional funds have a pressure to meet their target investment returns more so than institutional investors. So, they are looking for opportunities to raise rates to compensate for their higher risk factor.

- Private local and traditional funds have more flexibility than institutionally-backed funds. Whoever is more flexible and creative will win and will also command higher interest rates.

- Flexible local lenders are still lending, and they are extending loan terms by 90 days with the expectation they can take over national lenders who are caught with their pants down.

- $2 trillion dollars of stimulus is looming and inevitable. But there will be winners and losers. Global government stimulus is coming.

- All indications point to a restart of the economy in 60-90 days. Coupled with pressure for everyone to go back to being productive, we will see a bounce back.

- The realization is also starting to emerge that the sledge–hammer approach of locking everything down will do more harm than good, and saving a relatively lower percentage of people at the cost of a vast majority of people going homeless is not a solution. A surgical targeted approached in hot spots and in key demographic groups as well as wider testing will enable us to go back in 60-90 days to normal operations.

What's It All Mean?

Take a deep breath—the glass is still three-quarters full. The same money sources that are freezing the liquidity today will have pressures to lend and reinvest it instead of staying idle. They will have tighter guidelines, but that opens the market back up to the traditional private lenders and private funders, who will enjoy their wider margins.

Private lenders in local markets will know how to manage the risk better than national institutionally-backed lenders. Those local lenders and will once again thrive and keep the private lender sector going.

The market is also seeing draw requests accelerate. This means there's an opportunity, at least in the short term, for laborers who lost their jobs to join that workforce, accelerating the completion of projects. With $2 trillion dollars of stimulus coming in the U.S.—and the rest of the world looking at similar measures—the current situation will dissipate faster than people anticipate. Yes, it will mean higher rates, tightening of LTV and ARV, but also it means a reasonably healthy restart of the economy in 60-90 days.

And don't forget, prior to the emergence of the coronavirus, for the private lending industry, perhaps the biggest impact we have seen is that the industry grew up during the last several years. It has emerged from its infancy and started to mature.

Institutional capital started to flow to the space, providing liquidity to brokers and local lenders. This most notably created a totally new market for long–term finance of rental single and multiunit development and rehab.

To put things in perspective, according to Beacon Economics, the western markets' rental A space housing outpaced B and C units, growing 4% last year. Additionally, there was a decline in single–family rentals by 546,287 units and an increase in multiunit demands to 542,952. And, an additional 297,379 multiunits were purchased directly for owner occupancy.

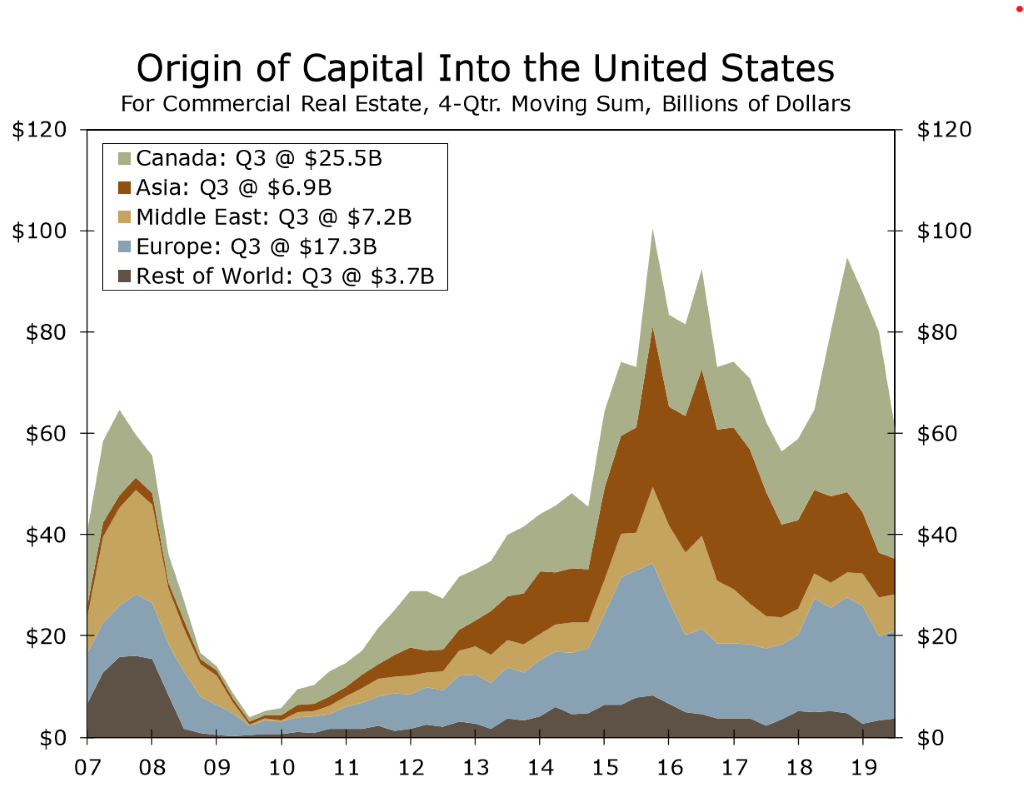

Now, if you are wondering where this new capital is entering the U.S. market from, the answer may surprise you. As you can see, Canada tops the charts.

Correlating Industry Data

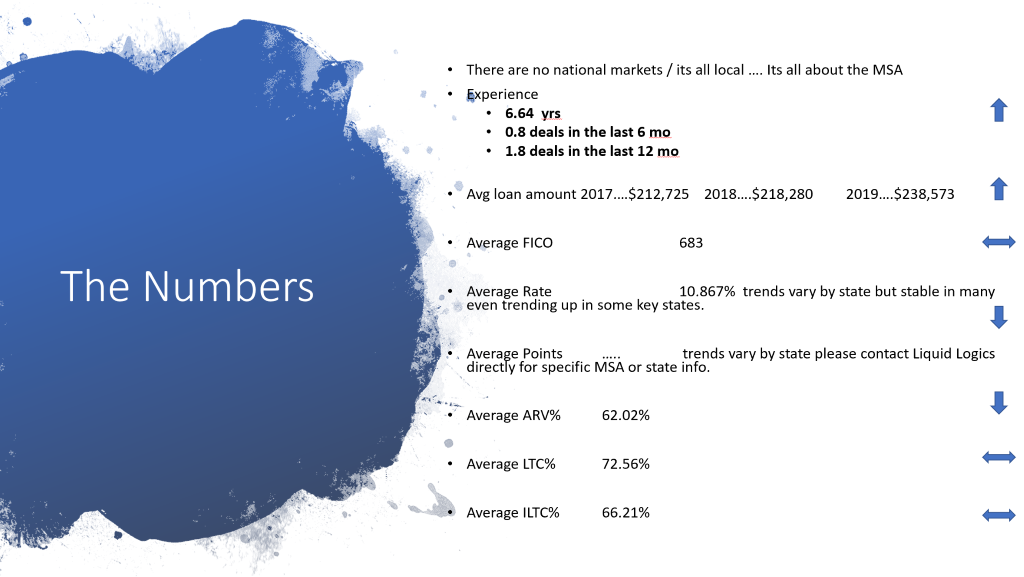

Last year at the AAPL national conference, we correlated data for the industry to share a general insight and trends. The fact is, while people talk about rate compression, the trends reveal the opposite in many markets while the rest held steady. Only in certain pockets, like California, are we seeing declining markets. While some argue it is because of competition in larger markets and states, the numbers in Texas and Carolinas show independence of the market size and an uptick in the rates and points. But the national average stands at the end of last year at 10.867%.

In contrast, mortgage rates have dropped nearly 135 basis points since the most recent peak on November 2018. They are down 100 basis points since this time last year.

The 15-year fixed rate fell to 3.05%, down from 4.05% a year ago. The 30-year jumbo rate fell from 4.04% to 3.96%, with 0.26 points.

All this is clearly a strong indicator why institutional investors are interested in adding a private lending portfolio backed by real estate portfolio. The returns simply are too attractive to ignore.

Those numbers, while accurate nationally, do not represent a specific local market.

Leave A Comment