Environmental contaminants can significantly decrease a property’s value and open both borrowers and lenders to liability. Here’s how to screen, evaluate, and mitigate impacts.

Environmental due diligence is the process of evaluating and identifying environmental risk associated with real estate collateral. Lenders require it to be performed for a variety of reasons, including the impact of contamination on collateral value and the liability protections it affords. Many types of environmental due diligence tools are available.

We’ll review these reasons and tools in further detail.

Reasons for Due Diligence

Collateral value. One of the primary reasons lenders require environmental due diligence is to determine whether environmental contamination will have an effect on the collateral’s value.

Remediation of contamination is costly and can often far exceed the borrower’s capabilities or even the value of the property. Lenders want to ensure that a borrower is not going to be burdened with remediation obligations and cleanup costs that will affect their ability to repay a loan. In the worst-case scenario—a borrower default—the collateral may not be worth its appraised value due to environmental issues. Borrowers may have difficulty selling the contaminated site without a significant discount or indemnity.

Liability protections. Another important reason for performing environmental due diligence is it gives both the borrower and the lender Comprehensive Environmental Response, Compensation and Liability Act (CERCLA) protections when acquiring property. Historically, the current owner or operator of a contaminated property could be held responsible for its cleanup, regardless of when the contamination occurred. However, if a borrower performs a Phase I ESA prior to purchase and unknowingly acquires a property with contamination, the borrower can qualify for the “Innocent Landowner Defense” to liability, assuming they follow their other obligations. In addition, lenders are granted secured creditor liability exemptions under CERCLA with the caveat they are not directly engaged in the management of a property during the course of a loan.

Even so, in the event contamination exists, these exemptions don’t protect either party from the reduction in property value that may occur. It is important to keep in mind that potential expenses may extend beyond remediation costs and can include expenses related to preventing exposures, third-party agreement transfer of environmental cleanup liability to the borrower, legal claims for cleanup or other damages, consent or administrative order obligations, expenses related to unacceptable exposure from site operations, and compliance fees or other violations.

Due Diligence for Lender Underwriting

Private lenders are less strictly regulated than banks and other traditional lenders in the Federal Reserve system. Accordingly, they often have more intrinsic flexibility and can have less built-in policy around environmental due diligence, which leads to a varied approach. Whatever the approach, the primary focus should be to identify existing and potential environmental liabilities that could divert the borrower’s cash flow.

As noted, developing environmental policies and procedures should be integral for every lender to ensure a loan can be repaid and that assets or guarantees pledged are sufficient to cover the loan amount in the event of default. The foundation of a good, well-balanced environmental policy takes into consideration the following three categories:

- Type of loan (e.g., new loan, renewal, refinance, foreclosure, etc.)

- The property’s collateral risk category (e.g., property type, including current and historical uses)

- Loan amount

Due diligence often differs based on those three categories. For example, the level of due diligence conducted for a refinance on a multifamily development with robust prior due diligence may differ from due diligence conducted for a new loan for an auto repair facility with lengthy operations or a strip mall with a dry-cleaner tenant. The goal of proactive due diligence is to prevent default. All due diligence should be conducted with the goal of being able to divest of a property in the event of default without taking losses due to a costly environmental issue.

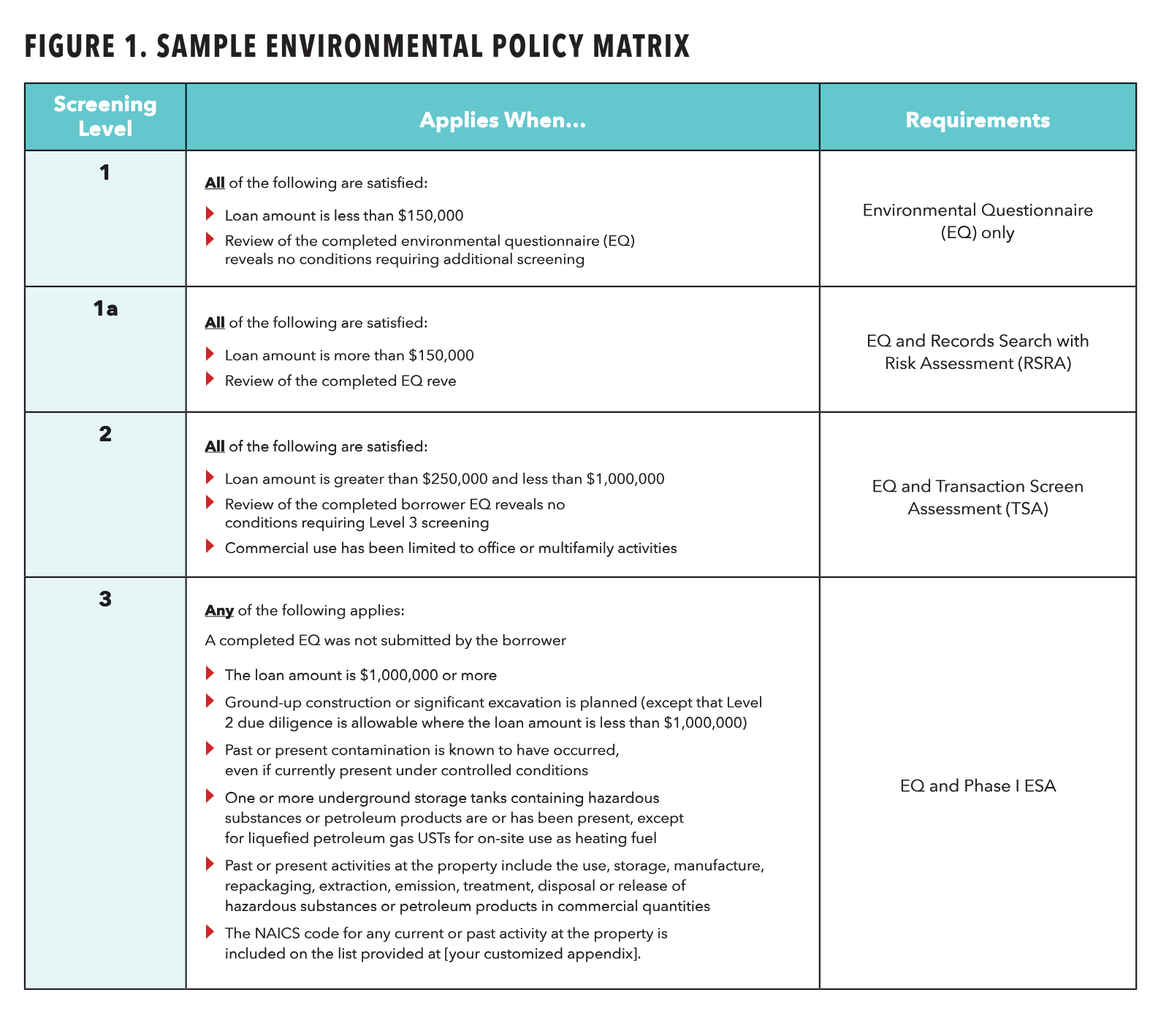

A well-written policy provides lenders with a due diligence process tailored to their carefully outlined risk tolerance. Figure 1 shows an example of an environmental policy matrix that clearly defines screening levels and offers a tiered approach to reporting requirements.

Let’s take a closer look at category No. 2 in the previous list: property types and features. The environmental risk of collateral is often determined by its current and historical uses. There are several uses known to be environmentally risky. Historical use is sometimes more problematic, especially if these uses were conducted prior to modern regulatory oversight, which is generally considered to have commenced in the early 1980s.

Understanding these uses and the potential risks they present can help guide the environmental due diligence process from the beginning stages. Lenders often use the NAICS Codes of Environmentally Sensitive Industries (currently found in Appendix 6 of SBA’s SOP 50 10 6) to determine the risk associated with a property type or use.

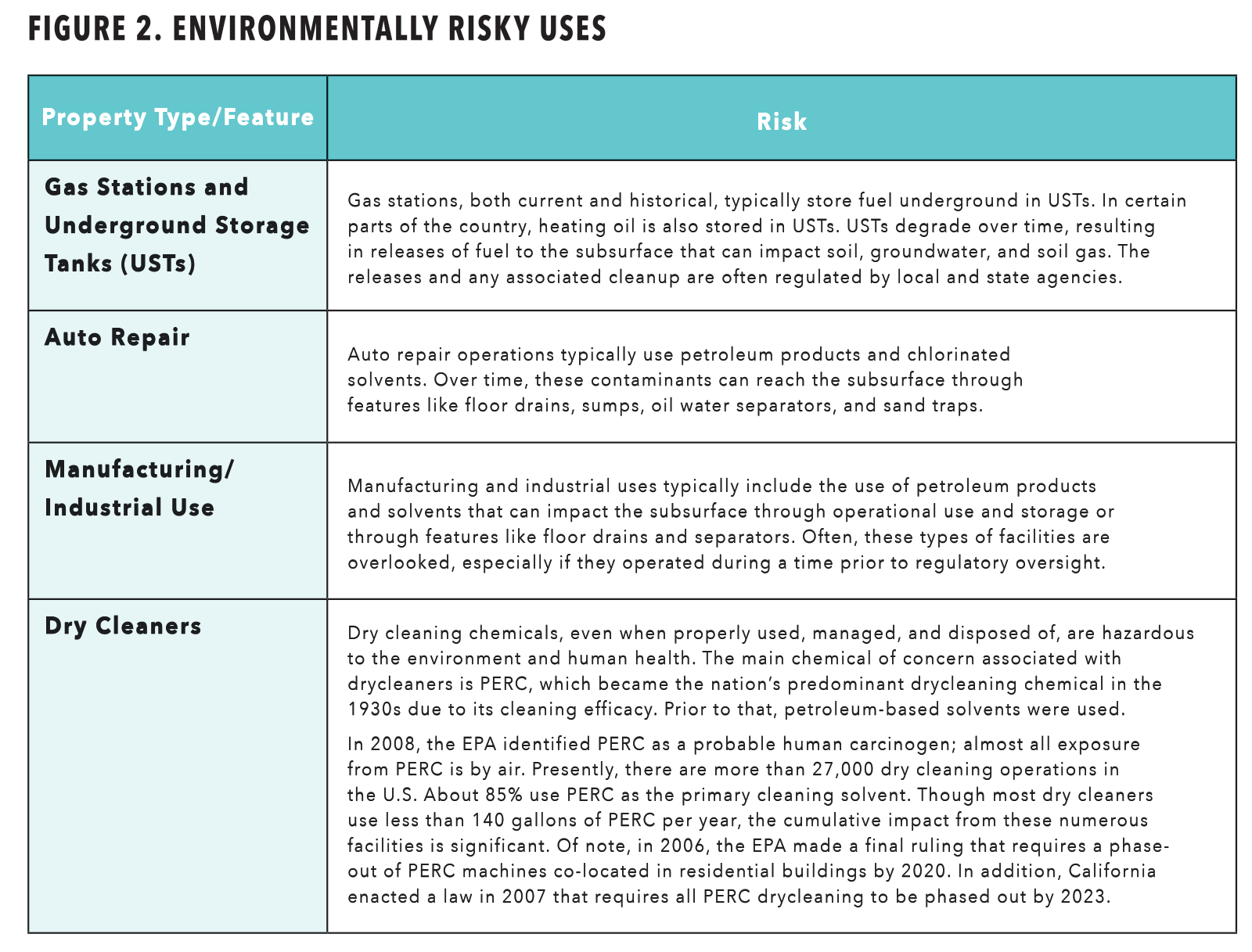

Some of the more common environmentally risky uses are described in Figure 2.

It is also important to be aware that environmental liabilities can originate from off-site sources. Off-site issues can include regional groundwater plumes, dry cleaners, gas stations, and other commercial and industrial properties that might impact occupants. Off-site issues can often cause a threat to human health that can be equal to or exceed an on-site issue. It may be surprising to learn that an environmental issue that didn’t even originate on your property could pose a threat; however, it is important to remember that contamination travels beneath the ground surface through groundwater and through the air spaces that exist between soil particles.

Environmental Due Diligence Tools

There are many types of environmental due diligence tools and many ways to perform it. The most diligent are Phase I and Phase II ESA. They lower liability and manage risk for the stakeholders involved. But not all loans require or warrant full Phase I and II ESA for underwriting purposes.

A tiered approach to environmental due diligence involving streamlined environmental reports that are more limited in scope can be a cost-effective and efficient tool for screening some properties. These types of reports are often used for smaller loans or loans involving lower-risk properties.

Phase I ESA. The gold standard is the Phase I Environmental Site Assessment (ESA) conducted in accordance with the current ASTM 1527-21, with the goal of identifying the presence or likely presence of contamination. Many lenders rely on a Phase I ESA to determine the impact, or potential impact, of environmental contamination on a collateral’s value and to identify liability exposure.

Environmental concerns identified during the due diligence process can represent significant risk exposure. Using the ASTM 1527-21 standard is important because it meets the Environmental Protection Agency’s (EPA) All Appropriate Inquiry (AAI) requirements and provides CERCLA liability protection to the user, as noted previously.

Phase II ESA. When a Phase I ESA identifies a recognized environmental condition (REC) or the potential for impacts at a property, the next step is to evaluate the presence, or absence, of contaminants in the subsurface of a property. This is done by performing a Phase II ESA, or subsurface investigation, which tests soil, soil gas, and/or groundwater to identify sources of environmental impacts. A Phase II ESA can help determine liabilities and long-term costs associated with a property.

Environmental Questionnaire (EQ). The environmental questionnaire was developed for Small Business Administration (SBA) loans, but it has been adopted in the ASTM E1527 Phase 1 Standard and can be a sound way for a lender to initially screen for risk. The EQ allows smaller loans on less risky properties to get by without doing comprehensive environmental due diligence—at least at first. If the loan amount is under a predetermined threshold and the site use is not listed as an environmentally sensitive operation, the EQ is a great place to start. The EQ is typically filled out by a lender who has visited the property and by an owner or occupant. If the EQ identifies any risk, a higher level of due diligence is usually required.

Transaction Screen Assessment (TSA) Report. A TSA is a cost-effective limited environmental due diligence report, but slightly more detailed in scope than the RSRA report (see below) and does require a site visit. It is essentially a scaled down version of the Phase I ESA; however, it follows an alternative ASTM method (E1527-14). A TSA report is appropriate for lower risk properties. Because it adheres to an alternative standard, the TSA does not meet the requirements of the EPA’s AAI and will not offer the borrower protection from CERCLA liability.

Records Search with Risk Assessment (RSRA) Report. Sometimes a lender may begin due diligence with an RSRA report, or it may be performed after an EQ is completed. An RSRA is performed by an Environmental Professional (EP) who assesses whether a property is at low risk or high risk for contamination based on a records search. It includes a search of government databases and a search of historical use records dating back to 1940 or first developed use. It should be noted that the RSRA does not include a visit to the collateral or any interviews. This report is often appropriate in refinance situations, low dollar amount loans, or low-risk category properties.

For any of the previously described reports, if a significant environmental concern is identified, then the evaluation may be elevated to a more comprehensive report such as the Phase I ESA. If further investigation is warranted, some EPs will offer a full credit of fee paid to go toward the Phase I ESA.

Developing Your Own Environmental Screening Policy

Environmental due diligence is an important step for both lenders and borrowers. It protects the real estate collateral’s value and prevents any liability for contamination in the future. In addition, if contamination is found, environmental due diligence can help the buyer decide whether to purchase the asset or request a commensurate reduction in price.

Because each loan transaction may require a different approach, conducting due diligence early in the process can help prevent delays if issues arise. Knowing the property type and use may be beneficial, as it allows lenders to anticipate what due diligence is needed early in the underwriting process. For example, environmental policies often require both a Phase I and a Phase II ESA for properties with dry cleaners or gas stations. In the event both reports are needed in a timely manner, some EPs may be able to offer semi-concurrent Phase I and II reports.

Remember, when conducting environmental due diligence, it’s important to work with experienced environmental professionals who provide thorough reports and understand the needs of your institution and its reporting requirements.

Financial Impact of Environmental Contamination

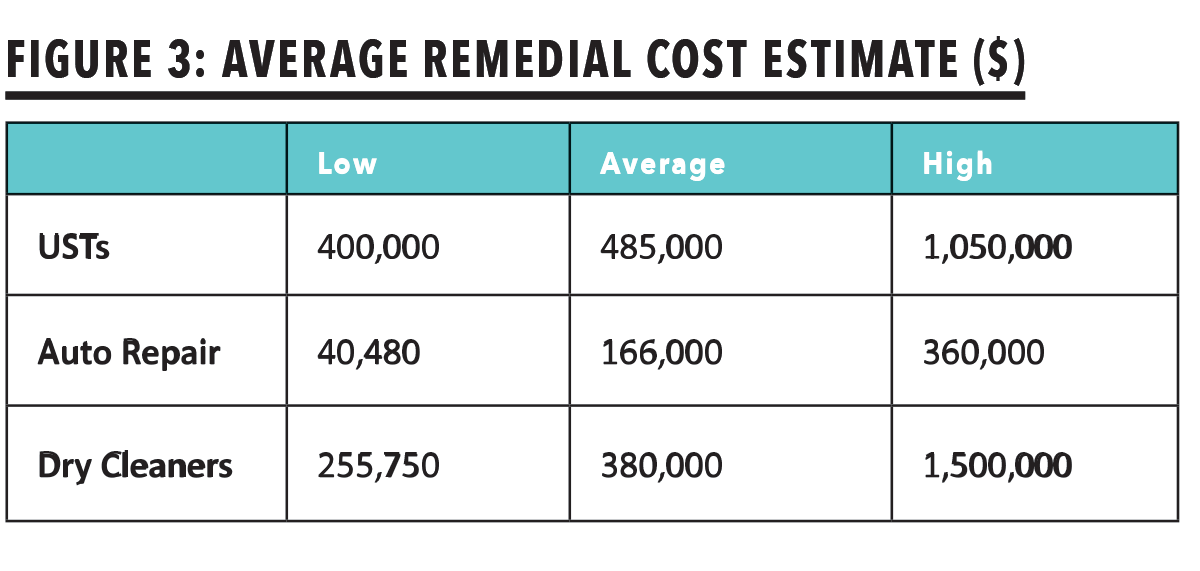

The presence of a recognized environment condition (REC) or impact from completion of one of the reports discussed previously can greatly reduce a property’s value. When contamination is identified, several tools are available to help determine next steps that can assist in the credit risk decision-making process for a particular loan. For example, a Remedial Cost Estimate, which is tailored to an individual property, can provide a potential range of costs associated with remediating a property. Having these costs in hand when underwriting a loan on collateral with documented contamination is imperative, because it can guide the lender in decision-making around loan-to value-ratios and potential amounts to be set aside to cover future cleanup costs and related expenses.

Remedial costs associated with environmental contamination can vary greatly. Often, costs can be significant, depending on the type and extent of contamination and use of the property. The presence of contamination does not always translate into a dead deal. Some environmental issues are easily addressed, but understanding the costs associated with these issues is imperative. Figure 3 is an analysis of 145 remedial cost reports of the more significantly risky property uses. Having a remedial cost estimate developed for a contaminated property will help you accurately identify the borrower’s ability to address the problem while maintaining solvency.

Remedial costs associated with environmental contamination can vary greatly. Often, costs can be significant, depending on the type and extent of contamination and use of the property. The presence of contamination does not always translate into a dead deal. Some environmental issues are easily addressed, but understanding the costs associated with these issues is imperative. Figure 3 is an analysis of 145 remedial cost reports of the more significantly risky property uses. Having a remedial cost estimate developed for a contaminated property will help you accurately identify the borrower’s ability to address the problem while maintaining solvency.

The remedial cost estimates in the table consist of the cost to investigate and remediate a site, but they do not include other significant costs, damages, and other expenses such as loss of revenue due to inhabitability of the site, stigma damages, diminution in value, potential liability associated with the contamination migrating beyond the boundaries of the site, and implicating property damage claims from adjacent landowners.

Many lenders require borrowers to resolve contamination issues prior to loan closing, especially those that may be costly or involve the approval of regulatory agencies. Some environmental provisions can be post-closing events, however. This may be the case when thorough due diligence has been conducted and an understanding of the risk informs loan structure in a proactive way that incentivizes a borrower to complete the required post-closing actions.

The post-closing process in these cases should include setting an escrow amount that addresses the remedial needs of the property and provides a reasonable contingency relative to the risk, including cost and time budget. The amount of equity in the loan, the strength of the borrower and their level of experience with similar projects, and the level of comfort relative to the level of risk should all be taken into consideration.

It is also important to clearly identify all requirements in the loan terms, including timelines and borrower deliverables, scopes of work and/or regulatory action plans, and provide clear timeframes for work to be completed.

Leave A Comment